Financial Statement Analysis

Anyone

wishing to study this textbook can learn valuable insights about

accounting. Does the mere fact that this book exists mean that everyone

knows about accounting principles? Obviously not. By analogy, the same

can be said about financial information. Many companies spend

substantial amounts of money preparing and presenting financial

statements that are readily available(the reports for USA public

companies can be found at www.sec.gov).

Does this mean that everyone has in-depth knowledge about these

companies? Again, no. Some degree of study is required to benefit from

the information.

Anyone

wishing to study this textbook can learn valuable insights about

accounting. Does the mere fact that this book exists mean that everyone

knows about accounting principles? Obviously not. By analogy, the same

can be said about financial information. Many companies spend

substantial amounts of money preparing and presenting financial

statements that are readily available(the reports for USA public

companies can be found at www.sec.gov).

Does this mean that everyone has in-depth knowledge about these

companies? Again, no. Some degree of study is required to benefit from

the information.It is important to know that CPAs and the SEC provide safeguards to protect the integrity of reported information, but this is entirely different than suggesting that reporting companies are necessarily good investments. For example, a company could report that its revenue stream is in decline, expenses are on the rise, and significant debt is coming due without a viable plan for making the payments. The financial statements may fully report this predicament. But, if financial statement users choose to ignore that report, only they are to blame.

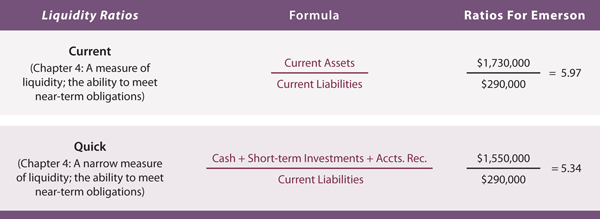

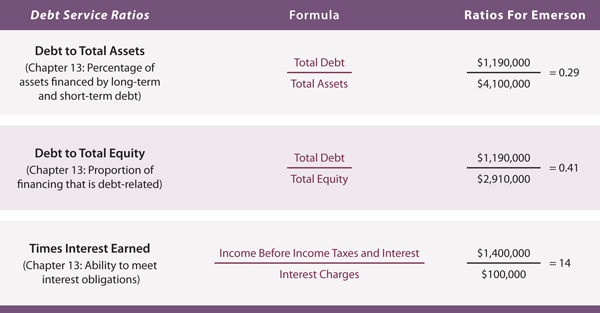

Investors must be very thorough in examining the financial statements of companies in which they are considering making an investment. Sometimes, the evaluation of complex situations can be assisted by utilization of key metrics or ratios. For example, a doctor will consider a patient’s health by taking measurements of blood pressure, heart rate, cholesterol level, and so forth. Likewise, consideration of a company’s health can be measured with certain important ratios.

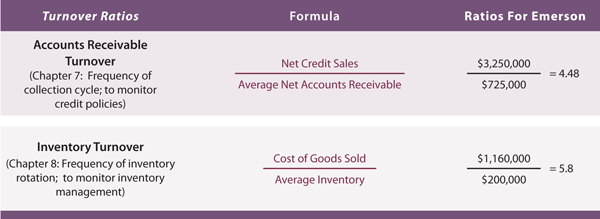

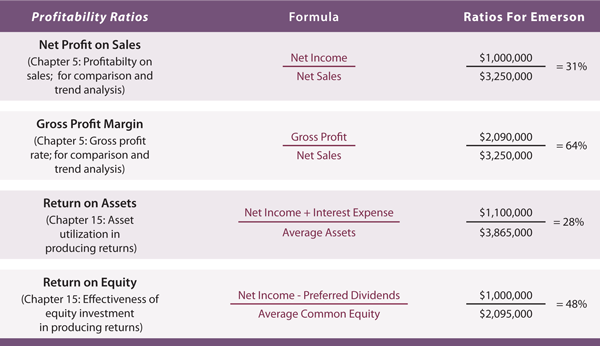

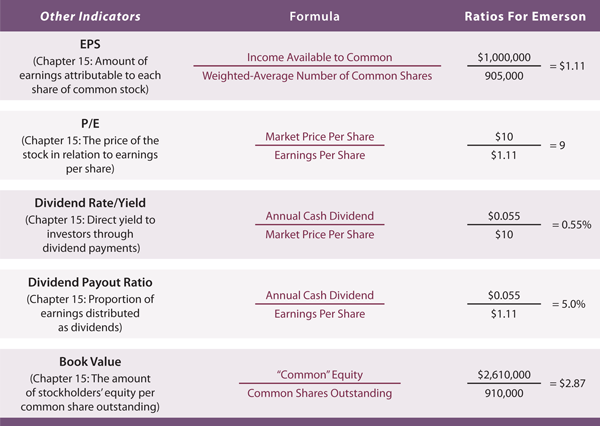

This book has introduced financial statement ratios and analysis techniques throughout many of the previous chapters. The following tables include a recapitulation of those ratios, including cross references back to chapters where the ratios were first introduced. If any of the ratios are unclear, it may prove helpful to refer back to the earlier chapters for more detail on the calculation and interpretation of the ratios. The right hand column of the tables include specific calculations for Emerson Corporation. Comprehensive financial statements for Emerson follow the tables. Be sure to verify each ratio calculation to the data included in those financial statements.

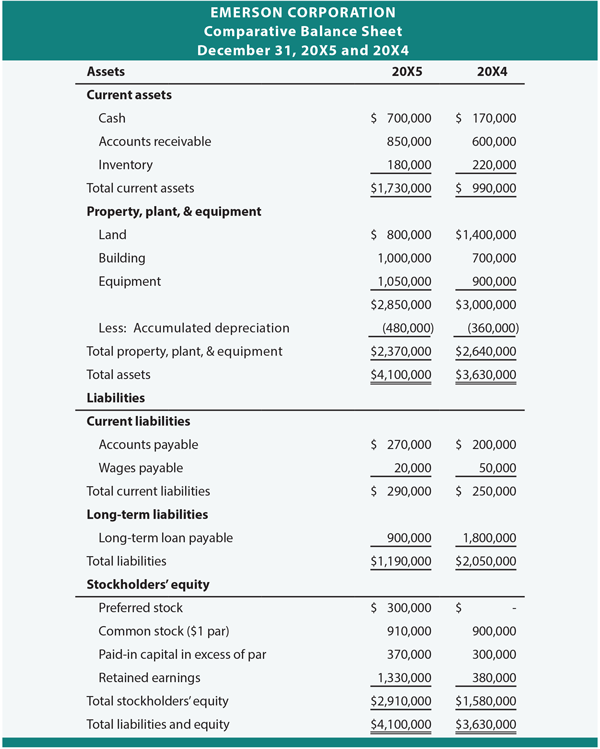

balance Sheet

additional facts for emerson

No dividends were due or paid on the $300,000 of preferred

stock which was issued in exchange for a building in late 20X5. Average

common equity is assumed to be $2,095,000 ((($2,910,000 - $300,000) +

$1,580,000)/2). Assume most other balance sheet items change uniformly

throughout the year (e.g., average receivables = ($600,000 + $850,000)/2

= $725,000, etc.). The year-end market value of the common stock was

$10 per share, and the cash dividend was paid on shares outstanding at

the end of the year ($50,000/910,000 shares = $0.055 per share).It appears that Emerson is doing fairly well. Its liquidity suggests no problem in meeting obligations, the debt is manageable, receivables and inventory appear to be turning well, and profits are good.

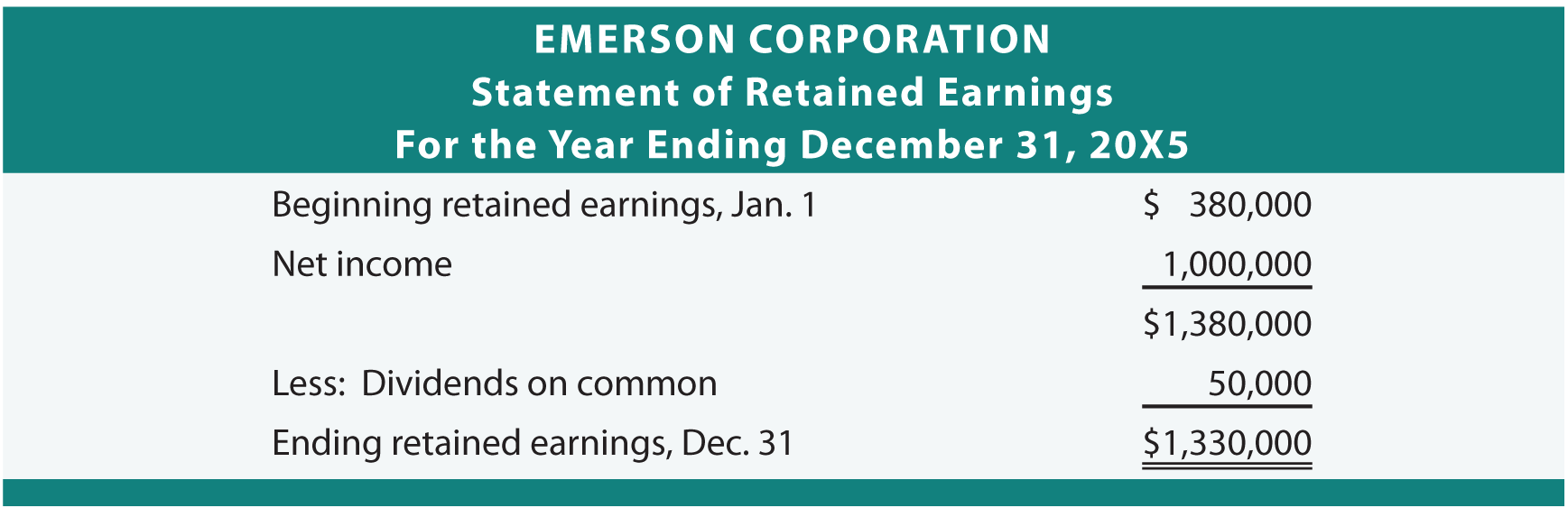

statement of retained earnings

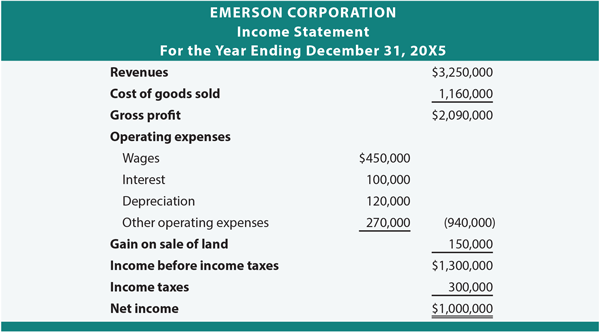

Income statement

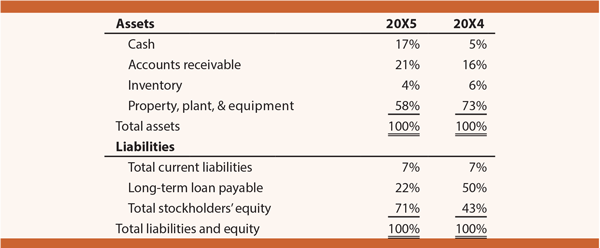

TREND ANALYSIS

Analysts often reproduce financial statement data in

percentage terms. For example, Emerson’s cash is 17% of total assets

($700,000/$4,100,000). These data provide investors and managers with a

keen sense of subtle shifts that can foretell changes in the business

environment. This approach is sometimes called “common size” financial

statements, as applied to the balance sheet data below:

Accounting is based upon accrual concepts that report revenues as earned and expenses as incurred, rather than when received and paid. Accrual information is perhaps the best indicator of business success or failure. However, one cannot ignore the importance of cash flows.

For example, a rapidly growing successful business can be profitable and still experience cash flow difficulties in trying to keep up with the need for expanded facilities and inventory. On the other hand, a business may appear profitable, but may be experiencing delays in collecting receivables, and this can impose liquidity constraints. Or, a business may be paying dividends, but only because cash is produced from the disposal of core assets. Sophisticated analysis will often reveal such issues.

Rather than depending upon financial statement users to do their own detailed cash flow analysis, the accounting profession has seen fit to require another financial statement that clearly highlights the cash flows of a business entity. This required financial statement is appropriately named the Statement of Cash Flows.

One objective of financial reporting is to provide information that is helpful in assessing the amounts, timing, and uncertainty of an organization’s cash inflows and outflows. As a result, the statement of cash flows provides three broad categories that reveal information about operating activities, investing activities, and financing activities. In addition, businesses are required to reveal significant noncash investing/financing transactions.

OPERATING, INVESTING, AND FINANCING ACTIVITIES

Cash inflows from operating activities

consist of receipts from customers for providing goods and services,

and cash received from interest and dividend income (as well as the

proceeds from the sale of “trading securities”). Cash outflows consist

of payments for inventory, trading securities, employee salaries and

wages, taxes, interest, and other normal business expenses. To

generalize, cash from operating activities is generally linked to those

transactions and events that enter into the determination of income.

However, another way to view “operating” cash flows is to include

anything that is not an “investing” or “financing” cash flow.Cash inflows from investing activities result from items such as the sale of longer-term stock and bond investments, disposal of long-term productive assets, and receipt of principal repayments on loans made to others. Cash outflows from investing activities include payments made to acquire plant assets or long-term investments in other firms, loans to others, and similar items.

Cash inflows from financing activities include proceeds from a company’s issuance of its own stock or bonds, borrowings under loans, and so forth. Cash outflows for financing activities include repayments of amounts borrowed, acquisitions of treasury stock, and dividend distributions.

There are potential distinctions between US GAAP and international accounting standards. IFRS permits interest received (paid) to be disclosed in the investing (financing) section of a cash flow statement. The global viewpoint also provides more flexibility in the classification of dividends received (and paid). Additionally, international standards encourage disclosures of cash flows that are necessary to maintain operating capacity, versus cash flows attributable to increasing capacity.

Some investing and financing activities occur without generating or consuming cash. For example, a company may exchange common stock for land or acquire a building in exchange for a note payable. While these transactions do not entail a direct inflow or outflow of cash, they do pertain to significant investing and/or financing events.

Under US GAAP, the statement of cash flows includes a separate section reporting these noncash items. Thus, the statement of cash flows is actually enhanced to reveal the totality of investing and financing activities, whether or not cash is actually involved. The international approach is to present such information in the notes to the financial statements.

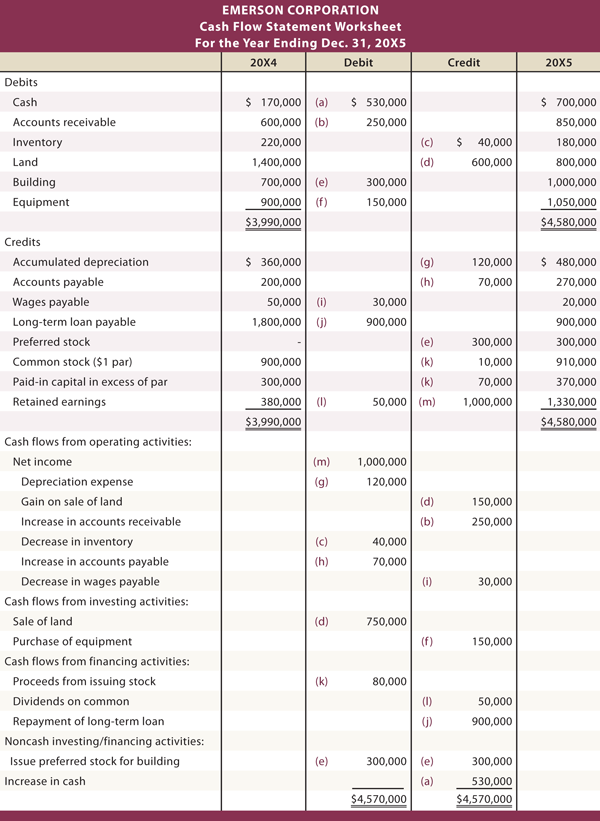

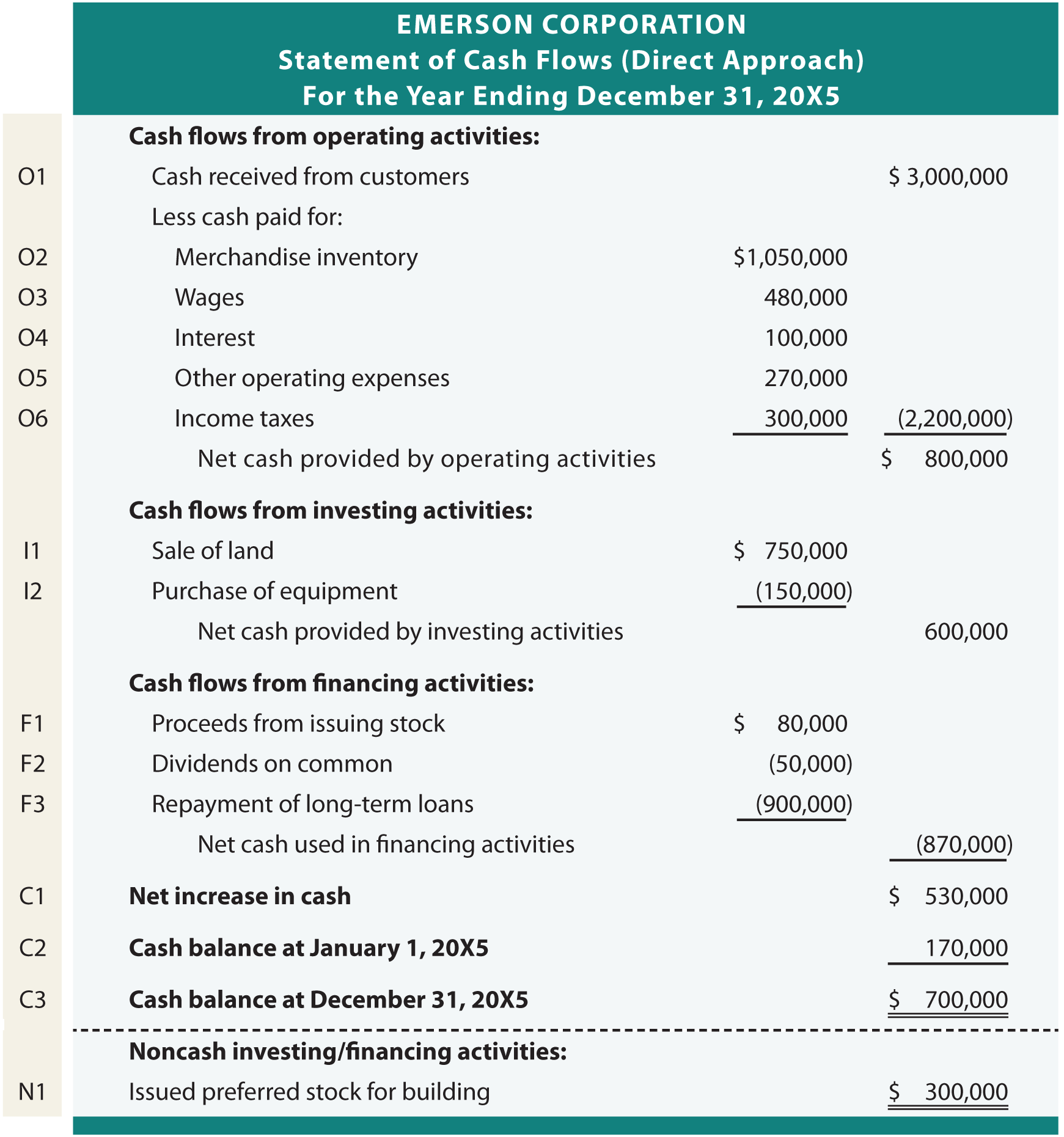

Spend just a few moments reviewing the preceding balance sheet, statement of retained earnings, and income statement for Emerson Corporation. Then, examine the following statement of cash flows. Everything within this cash flow statement is derived from the data and additional comments presented for Emerson. The tan bar on the left is not part of the statement; it is to facilitate the “line by line” explanation that follows.

Cash Received From Customers

=

Total Sales Minus the Increase in Net Receivables (or, plus a decrease in net receivables)

=

$3,250,000 - ($850,000 - $600,000)

=

$3,000,000

Accounts receivable increased by $250,000 during the

year ($850,000 - $600,000). This means that of the total sales of

$3,250,000, a net $250,000 went uncollected. Thus, cash received from

customers was $3,000,000. If net receivables had decreased, cash

collected would have exceeded sales.

Inventory Purchased

=

Cost of Goods Sold Minus the Decrease in Inventory (or, plus an increase in inventory)

=

$1,160,000 - ($220,000 - $180,000)

=

$1,120,000

Inventory purchased is only the starting point for

determining cash paid for inventory. Inventory purchased must be

adjusted for the portion that was purchased on credit. Notice that

Emerson’s accounts payable increased by $70,000 ($270,000 - $200,000).

This means that cash paid for inventory purchases was $70,000 less than

total inventory purchased:

Cash Paid for Inventory

=

Inventory Purchased Minus the Increase in Accounts Payable (or, plus a decrease in accounts payable)

=

$1,120,000 - ($270,000 - $200,000)

=

$1,050,000

Cash Paid for Wages

=

Wages Expense Plus the Decrease in Wages Payable (or, minus an increase in wages payable)

=

$450,000 + ($50,000 - $20,000)

=

$480,000

Emerson not only paid out enough cash to cover wages

expense, but an additional $30,000 as reflected by the overall decrease

in wages payable. If wages payable had increased, the cash paid would

have been less than wages expense.

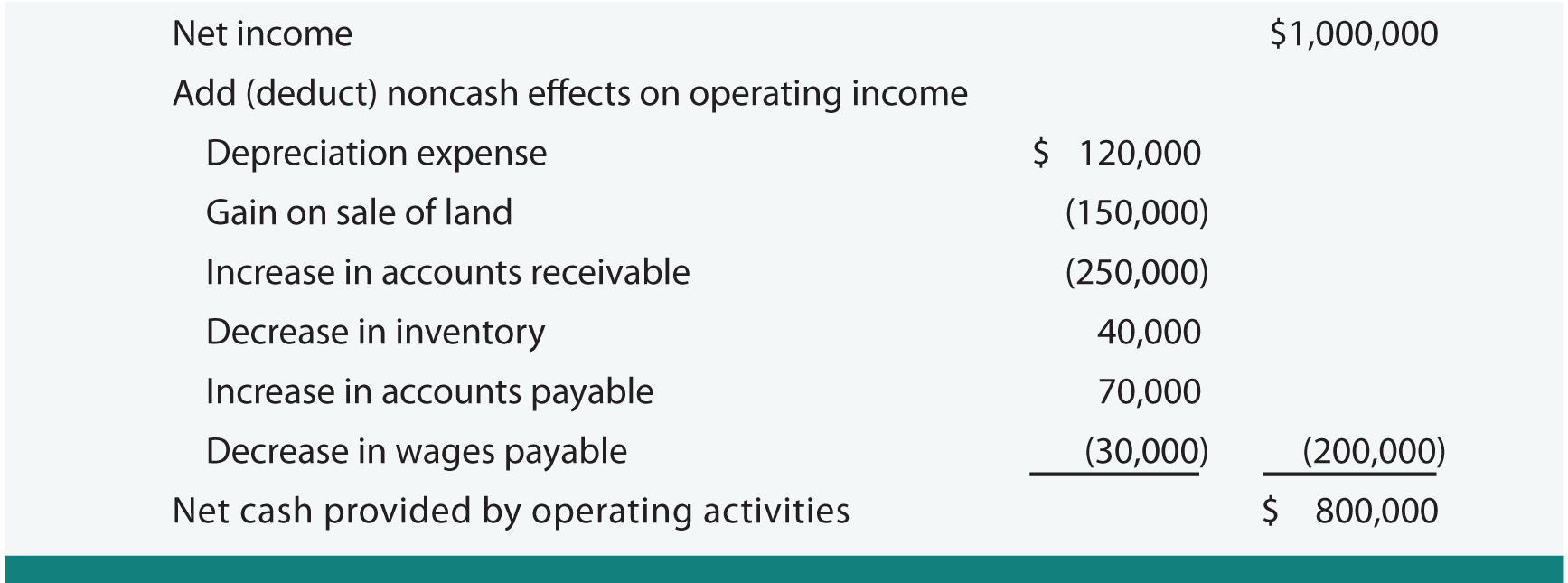

Overall, operations generated net positive cash flows of $800,000. Notice that two items within the income statement were not listed in the operating activities section of the cash flow statement:

- Depreciation is not an operating cash flow item. It is a noncash expense. Remember that depreciation is recorded via a debit to Deprecation Expense and a credit to Accumulated Depreciation. No cash is impacted by this entry (the “investing” cash outflow occurred when the asset was purchased), and

- The gain on sale of land in the income statement does not appear in the operating cash flows section. While the land sale may have produced cash, the entire proceeds will be listed in the investing activities section; it is a “nonoperating” item.

INVESTING ACTIVITIES

The next major section of the cash flow statement is

the cash flows from investing activities. This section can include both

inflows and outflows related to investment-related transactions. Emerson

Corporation had one example of each; a cash inflow from sale of land,

and a cash outflow for the purchase of equipment. The sale of land

requires some thoughtful analysis. Notice that the statement of cash

flows for Emerson reports the following line item:

FINANCING ACTIVITIES

CASH FLOW RECAP

NONCASH INVESTING/FINANCING ACTIVITIES

The statement of cash flows just presented is known as the direct approach. It is so named because the cash items entering into the determination of operating cash flow are specifically identified. In many respects, this presentation of operating cash flows resembles a cash basis income statement.

An acceptable alternative is the “indirect” approach. Before moving on to the indirect approach, be aware that companies using the direct approach must supplement the cash flow statement with a reconciliation of income to cash from operations. This reconciliation may be found in notes accompanying the financial statements:

- Depreciation is added back to net income, because it reduced income but did not consume any cash.

- Gain on sale of land is subtracted, because it increased income, but is not related to operations (remember, it is an investing item and the “gain” is not the sales price).

- Increase in accounts receivable is subtracted, because it represents uncollected sales included in income.

- Decrease in inventory is added, because it represents cost of sales from existing inventory (not a new cash purchase).

- Increase in accounts payable is added, because it represents expenses not paid.

- Decrease in wages payable is subtracted, because it represents a cash payment for something expensed in an earlier period.

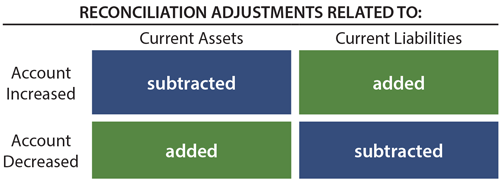

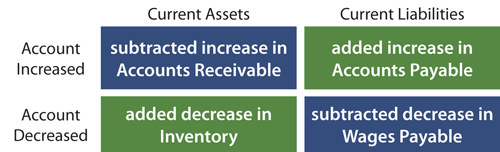

The following drawing is useful in simplifying consideration of how changes in current assets and current liabilities result in reconciliations of net income to operating cash flows. Begin by thinking about a reconciling item that is fairly easy to grasp. Emerson’s accounts receivable increased on the balance sheet, but the amount of the increase was subtracted in the reconciliation (again, this increase reflects sales not yet collected in cash, and thus the subtracting effect). In the drawing below, consider that accounts receivable is a current asset, and it increased. This condition relates to the upper left quadrant; hence the increase is shown as “subtracted.”

Although accounting standards encourage the direct approach, most companies actually present an indirect statement of cash flows. The indirect approach is so named because the “reconciliation” replaces the direct presentation of the operating cash flows. Except for the shaded areas, this statement is identical to the direct approach. The first shaded area reflects the substitution of the operating cash flow calculations. The second shaded area reflects that the indirect approach must be supplemented with information about cash paid for interest and taxes.

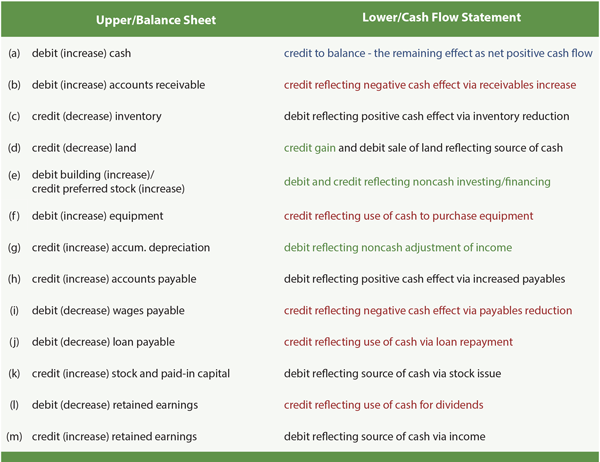

The worksheet examines the change in each balance sheet account and relates it to any cash flow statement impacts. Once each line in the balance sheet is contemplated, the ingredients of the cash flow statement will be found! A sample worksheet for Emerson is presented on the following page.

In this worksheet, the upper portion is the balance sheet information, and the lower portion is the cash flow statement information. The change in each balance sheet row is evaluated and keyed to a change(s) in the cash flow statement. When one has explained the change in each balance sheet line, the accumulated offsets (in the lower portion) reflect the information necessary to prepare a statement of cash flows.

Specific explanations for each keyed item in the worksheet are found in the following table. The cash flow statement explanations are color coded such that blue is the final balancing step, red is cash outflow, black is cash inflow, and green is special.